Why Las Vegas Multifamily Remains a Stabilizing Force in a Volatile Economy

Why Las Vegas Multifamily Remains a Stabilizing Force in a Volatile Economy

Economic turbulence defined 2025: rate volatility, tighter capital markets, and shifting renter behavior have made many investors ask the same question—where does stability still exist?

Multifamily continues to stand out because it’s supported by real-world demand, produces recurring cash flow, and can adjust faster than many other asset types. A recent Multi-Housing News analysis outlines several structural reasons apartments tend to hold up across cycles—and those same forces are showing up clearly in Southern Nevada.

Here’s how those national dynamics translate directly into the Las Vegas market.

1) New Supply in Las Vegas Is Pulling Back

Nationally, multifamily construction starts have fallen meaningfully from their recent peak—Yardi Matrix notes starts are about 40% below the 2022 peak, which typically leads to fewer deliveries ahead.

Las Vegas is already reflecting that slowdown in real numbers. Cushman & Wakefield reports the valley’s development pipeline contracted to 3,904 units under construction, down 49% from the Q2 2024 peak.

At the same time, Las Vegas has been digesting a large wave of recent deliveries—Institutional Property Advisors notes nearly 11,000 apartments were brought to market since year-end 2022, which has increased near-term competition and softened rent growth.

Why that matters: when supply growth slows after a delivery wave, competitive pressure often eases and fundamentals can tighten—especially in markets with household growth and in-migration tailwinds.

2) Homeownership Remains Out of Reach for Many Local Households

Las Vegas’s buyer affordability math is still tough for a large portion of the workforce. In November 2025, Clark County’s median home sale price was about $450,000.

Meanwhile, mortgage rates stayed elevated through much of the period—Freddie Mac’s weekly survey shows 30-year fixed rates in the mid-6% range in late 2025, after spending time near 7% earlier in the year.

Investor takeaway: when ownership costs stay high relative to incomes, the renter pool tends to deepen—not shrink—supporting long-term rental demand even when rents soften temporarily.

3) Renting Has Become a Lifestyle Choice, Not Just a Budget Constraint

Las Vegas also benefits from a “renter-by-choice” tailwind. Multi-Housing News cites a Harris Poll survey conducted for Credit Karma showing 58% of respondents said they live a “rent-first” lifestyle by choice, and 57% said flexibility matters more than ownership benefits.

That preference shows up locally in workforce mobility, job shifts, and lifestyle-driven location choices—factors that keep demand durable even when the market is noisy.

4) Multifamily Still Works as a Partial Inflation Hedge

Inflation and operating costs are real—so investors need assets that can adapt. Apartments have three structural advantages that matter in volatile periods:

-

Short-term leases that allow more frequent rent resets

-

Value-add potential through improvements and repositioning

-

Tax benefits such as depreciation that can reduce taxable income

In Las Vegas, value-add strategies can be particularly powerful when applied selectively—because performance varies dramatically by submarket, vintage, and unit mix.

5) Not All Multifamily in Las Vegas Performs the Same

This is where local expertise becomes non-negotiable. Multifamily is resilient as a category, but results vary by operator, location, and strategy—and even national commentary emphasizes the importance of sponsor quality and market selection.

Las Vegas data highlights that variation in real time:

-

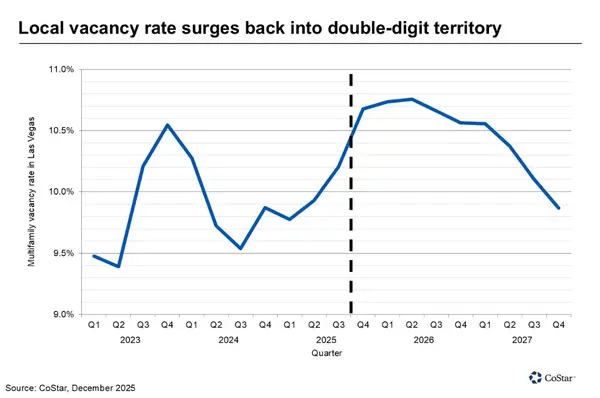

Q3 2025 vacancy was reported around 10.3%, with effective rents down year-over-year—reflecting the current supply digestion phase.

-

Demand has remained positive (continued absorption), even while new deliveries temporarily outpace it in certain quarters.

A lease-up in one submarket may behave nothing like a stabilized vintage asset across town. That’s why “valley-wide averages” can mislead—and why underwriting must be unit-type and comp-set specific.

The Las Vegas Bottom Line

Multifamily remains one of the most resilient investment categories available today—and in Las Vegas, the fundamentals supporting that resilience are especially clear:

-

the construction pipeline is shrinking

-

homeownership affordability remains strained

-

renter demand is supported by both necessity and preference

-

multifamily retains inflation-hedging mechanics through lease structure, value-add, and depreciation

-

submarket nuance creates opportunity for investors who underwrite precisely

Investors who approach this moment with discipline, local insight, and conservative underwriting can be well-positioned for the next tightening phase.

FAQ

Is Las Vegas multifamily “weak” right now because rents softened?

Not necessarily. Softening often reflects a temporary period of supply digestion. Las Vegas has absorbed a large delivery wave since year-end 2022 while the forward pipeline has been contracting.

Why does a shrinking construction pipeline matter so much?

Fewer starts today generally means fewer deliveries later. When new supply eases while demand remains steady, occupancy tightens and rent growth can recover.

What’s supporting renter demand in Las Vegas if the economy is choppy?

Affordability constraints in homeownership (price + rates) keep households renting longer, and a growing segment of renters prioritize flexibility as a lifestyle choice.

How do mortgage rates factor into multifamily performance?

Higher mortgage rates can reduce homebuyer demand and expand the renter pool. Freddie Mac’s survey shows rates remained elevated through much of 2025, supporting “rent longer” behavior.

Does multifamily really hedge inflation?

It can partially hedge because leases reset more frequently than many commercial contracts, owners can create value through improvements, and depreciation can reduce taxable income.

Why is submarket underwriting so important in Las Vegas?

Because performance varies sharply by neighborhood, vintage, and competitive set. Market-wide averages can hide the difference between a supply-heavy lease-up pocket and a stable, affordability-driven corridor.

What’s the smartest approach to acquisitions in this phase of the cycle?

Conservative underwriting: effective rent (after concessions), realistic expenses/turnover, DSCR stress tests, and a clear view of nearby future deliveries and competitive set behavior.

Categories

Recent Posts

GET MORE INFORMATION