What Recent Rent Declines in Las Vegas Really Mean for Investors

What Recent Rent Declines in Las Vegas Really Mean for Investors

Recent coverage in the Las Vegas Review-Journal is highlighting cooling rents—especially for one-bedroom units—across parts of the Las Vegas Valley. At a glance, that can read like “rental demand is weakening.”

The smarter takeaway is more specific: headline rent declines are a directional signal, not a property-level conclusion. In today’s market—where concessions, new deliveries, and dynamic pricing can distort averages—investors need to interpret rent headlines the same way they interpret cap rates: with context, segmentation, and verification.

What the Data Is Actually Signaling

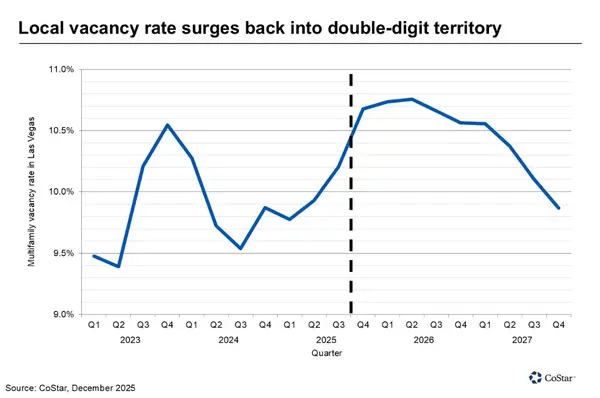

The Review-Journal reporting, based on a Zumper analysis, points to softening in certain pockets while other neighborhoods show rent increases. It also ties the cooling to a recent surge of new multifamily supply—more competition, more concessions, and slower rent growth in submarkets absorbing new deliveries.

The same pattern shows up in institutional market commentary: elevated recent deliveries can pressure vacancy and rent growth, while the construction pipeline is expected to cool as financing and building costs remain high, setting up tighter conditions later.

In plain terms: near-term softness + future supply slowdown is a very normal late-cycle setup.

What Headline “Median One-Bedroom Rent” Doesn’t Tell You

This is where investors can misread the market if they rely on a single metric.

Median one-bedroom rents:

-

Blend multiple property types (workforce apartments, Class A, condos, scattered SFR-style rentals marketed like apartments)

-

Ignore unit mix (a property dominated by 2–3BR units can perform differently than one heavy on 1BR)

-

Don’t separate effective rent from asking rent (concessions can materially change real income)

-

Can swing wildly in low-inventory areas (small one-bedroom count = exaggerated percentage moves)

-

Don’t reflect the competitive set (a 1988 vintage Class B in Spring Valley is not competing the same way as new Class A product)

So yes—some one-bed rents may be down. That does not automatically mean your target asset class, unit mix, or micro-location is down in the same way.

What This Means for Investors Right Now

1) The “pain” is uneven—and that’s where opportunity lives

New supply pressure tends to hit newer Class A first (and the Class B properties positioned closest to that Class A price band). Meanwhile, well-located Class B/C often holds up better when affordability becomes the main decision driver.

2) Underwrite effective rent, not advertised rent

In a concession-heavy environment, your real revenue is the lease-up reality:

-

effective rent (after concessions)

-

renewal spreads and lease expirations

-

vacancy burn-off timeline

-

true loss-to-lease by unit type

3) A thinning pipeline can flip leverage back to owners faster than people expect

A lot of investors get stuck thinking “rents are down” is the whole story. The more important cycle question is: how long does competition stay elevated? When starts slow and the pipeline thins, the market can tighten—even if the headlines haven’t caught up yet.

4) This is a negotiation market for disciplined buyers

Softness creates room for:

-

better basis

-

stronger terms

-

seller credits

-

capex budgets that actually match the property’s needs

If you’re conservative on income and realistic on expenses, you can buy assets that look average today but are positioned for upside as supply pressure eases.

How HYDE Real Estate Group Interprets Rent Headlines

Our approach is hyper-granular and deal-driven:

-

Unit-type specific analysis (not blended medians)

-

Submarket and micro-market comps (true competitive set)

-

Rent-roll stability and lease expiration risk

-

Effective rent and concessions (what’s collectible now)

-

Future supply risk (what’s delivering near the asset)

-

Demand drivers that are actually durable (jobs, access, affordability)

Headlines set context. The rent roll, the comp set, and the supply map decide the deal.

How to Move Forward With Clarity

If you’re acquiring, repositioning, or holding in Las Vegas, the best move right now is simple: replace broad assumptions with property-specific truth.

HYDE Real Estate Group supports investors with:

-

Deal review and underwriting (income, expenses, DSCR, break-even, capex realism)

-

Submarket rent/vacancy snapshots based on the actual competitive set

-

Current Class B/C value-add opportunities aligned with affordability-driven demand

FAQ

Are rent declines in Las Vegas a red flag for multifamily investors?

Not automatically. They often reflect new supply competition and concessions, and they may be concentrated in specific product types or neighborhoods rather than the entire market.

Why focus on one-bedroom data at all if it’s limited?

It’s still useful as a directional signal—especially for renter sentiment and competitive pressure—but investors should treat it as one input, not the underwriting conclusion.

What’s the biggest mistake investors make when reading rent headlines?

Assuming medians translate directly to their target asset. Medians blend different property classes, unit mixes, and locations—often hiding the real competitive story.

How do concessions change the real picture?

Concessions reduce effective rent, which impacts NOI, valuation, and debt coverage. Two properties can have the same asking rent but very different effective rent outcomes.

Which assets tend to hold up better during supply-heavy periods?

Often, well-located Class B/C in stable neighborhoods—because affordability drives demand and renters trade down when Class A pricing stays elevated.

What should I underwrite differently in a cooling rent environment?

Use conservative assumptions: effective rent (not asking), realistic vacancy/turnover, modest renewal growth, and stress tests on expenses and debt coverage.

Why does a thinning construction pipeline matter?

If starts slow and the pipeline shrinks, future deliveries drop—reducing competition and supporting tighter occupancy and rent recovery later.

What information do you need for a quick deal review?

Address, offering memo, current rent roll, trailing 12 (or T-3 annualized), and any renovation scope/pricing if it’s value-add. That’s enough to validate effective rent, expenses, DSCR sensitivity, and break-even occupancy.

Categories

Recent Posts

GET MORE INFORMATION