Finding Clarity in a Noisy Market: How HYDE Real Estate Secures Strong Deals Amid Negative Rent Growth

Finding Clarity in a Noisy Market: How HYDE Real Estate Secures Strong Deals Amid Negative Rent Growth

When national rent growth turns negative, a lot of investors freeze—or worse, they start “hoping” their way through underwriting. In this cycle, hope is expensive.

Across the U.S., rent declines and volatile lease pricing have disrupted the old acquisition playbook, while many sellers remain anchored to peak-era valuations—keeping transaction volume choppy and underwriting risk high.

Las Vegas isn’t immune to the national reset, but it is positioned to outperform as the next cycle takes shape—if buyers underwrite what’s real today, not what used to be normal.

At HYDE Real Estate Group, we’ve leaned harder into fundamentals that reward discipline: verified income, realistic expenses, conservative debt sizing, and downside protection built into every model.

The Rent Roll Comes First (Not the Pro Forma)

In a dynamic-pricing world, surface-level averages are no longer reliable. Lease rates can vary by $200–$300 for the same floor plan based on timing, expirations, and revenue management strategy—so “market rent” needs to be proven, not assumed.

That’s why we start with the rent roll and go line by line:

-

Identify lease anomalies and one-off concessions

-

Separate asking rent from effective rent

-

Normalize pricing to what the submarket is actually supporting right now

-

Validate leasing velocity (not just advertised rates)

This is underwriting like forensic accounting—because that’s what today’s market requires.

We Pressure-Test Every Assumption (Because NOI Is Getting Squeezed)

Rents aren’t the only variable. Expenses have been rising while renewals soften, which is leaving many operators “treading water” on NOI—even if occupancy looks fine on paper.

So we bake in downside protection from the start:

-

Fully loaded operating expenses (not “best case”)

-

Realistic turnover and loss-to-lease assumptions

-

Conservative rent growth (including flat scenarios)

-

Financing sensitivity (rate, DSCR, and exit assumptions)

-

Risk premiums that match the property and the submarket

We also verify key inputs with people closest to reality: property management partners, local housing dynamics, and our lending and insurance relationships—so the model reflects execution, not theory.

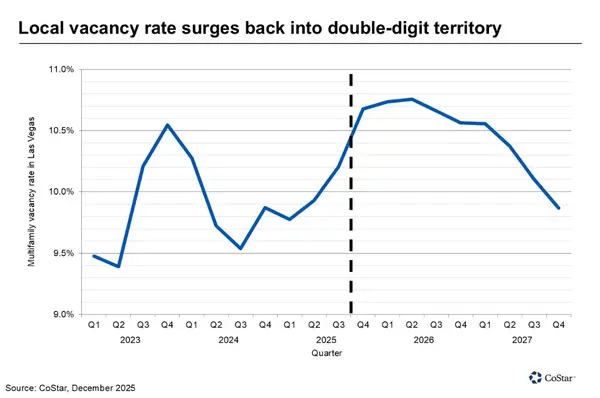

Submarket Reality Matters More Than Citywide Headlines

National headlines can be directionally useful, but Las Vegas is a patchwork market. Underwriting has to reflect how demand and affordability behave at the neighborhood level.

That’s why our models are grounded in true performance across Las Vegas submarkets where renter demand is consistently active—areas like Henderson, Southwest, Spring Valley, and North Las Vegas—with rent expectations tied to real absorption and competitive set behavior, not generic market averages.

Meanwhile, broader data continues to show national rent growth and occupancy trends moving in uneven waves, with supply-heavy markets feeling the pressure first and recovery timing varying by region.

Discipline Is the Edge When the Market Is Loud

In markets like this, the best investors aren’t the ones “swinging for upside.” They’re the ones avoiding avoidable mistakes—because downside can compound faster than upside can save you.

That theme is showing up nationally: conservative underwriting, income stability, and walking away from aggressive assumptions are becoming the new standard.

Our rule is simple: if a deal doesn’t clear evidence-based thresholds in today’s conditions, we pass. That willingness to step back is what lets us step forward decisively when the right opportunity shows up.

This is how HYDE Real Estate Group has stayed consistent through multiple cycles—and why we continue delivering strong outcomes even when the national narrative feels uncertain.

Work With HYDE Real Estate Group

If you want a team that can separate signal from noise in this market, we’re here to help. The path to good deals hasn’t disappeared—it has shifted.

Here are the three fastest ways we can support you right now:

-

Request a deal review / underwriting

Send the address + offering memo and we’ll break down effective rents, concessions, expense reality, DSCR sensitivity, break-even occupancy, and value-add upside (with timing you can trust).

-

Get a submarket rent & vacancy snapshot

Send 2–3 submarkets or zip codes and your target unit count, and we’ll outline rent pressure, vacancy direction, concessions, pipeline risk, and where B/C is actually holding up.

-

Ask for current B/C value-add opportunities

Send your buy box (price range + doors + preferred areas) and we’ll share active B/C opportunities worth underwriting—plus the most common operational upside angles we’re seeing.

FAQ

Why does negative rent growth change underwriting so much?

Because the traditional model relies on steady rent increases to “fix” thin margins. When rent growth is flat or negative, the deal has to work on today’s income and realistic expense assumptions, not future optimism.

Why are rent rolls harder to interpret now than before?

Dynamic pricing and revenue management tools can create wide spreads for identical units based on lease timing, expirations, and term length. That makes simple averages misleading and forces deeper rent-roll analysis.

What’s the biggest mistake buyers make in a concession-heavy market?

Underwriting off asking rents instead of effective rents. Concessions can materially change true income, and ignoring them can inflate NOI and overstate value.

How do you underwrite “market rent” when pricing is inconsistent?

We normalize rent-roll data by identifying anomalies, removing one-time distortions, comparing true effective rents across the comp set, and matching revenue expectations to actual leasing velocity—not just advertised rates.

Are sellers really still anchored to past valuations?

In many markets, yes. The bid-ask gap persists when sellers price off peak-era expectations while buyers price off today’s revenue reality—contributing to slower deal flow.

What’s the most important “downside protection” lever in underwriting right now?

A conservative NOI model: fully loaded expenses, realistic turnover, effective-rent assumptions, and debt sensitivity testing (especially DSCR and break-even occupancy).

Why can Las Vegas still outperform even with national softness?

Because performance is increasingly local. Submarket job bases, affordability, and supply pressure can diverge meaningfully from national averages—creating pockets where well-bought deals can still perform while broader sentiment stays cautious.

What should an investor send to get a deal reviewed quickly?

The address, offering memo, current rent roll, trailing 12 (or T-3 + annualized), and any renovation scope/pricing if it’s value-add. That’s enough to stress-test the deal and identify the real drivers.

Categories

Recent Posts

GET MORE INFORMATION