Headline Vacancies vs. Real Performance: Las Vegas Multifamily Tells a Stronger Story

Headline Vacancies vs. Real Performance: Las Vegas Multifamily Tells a Stronger Story

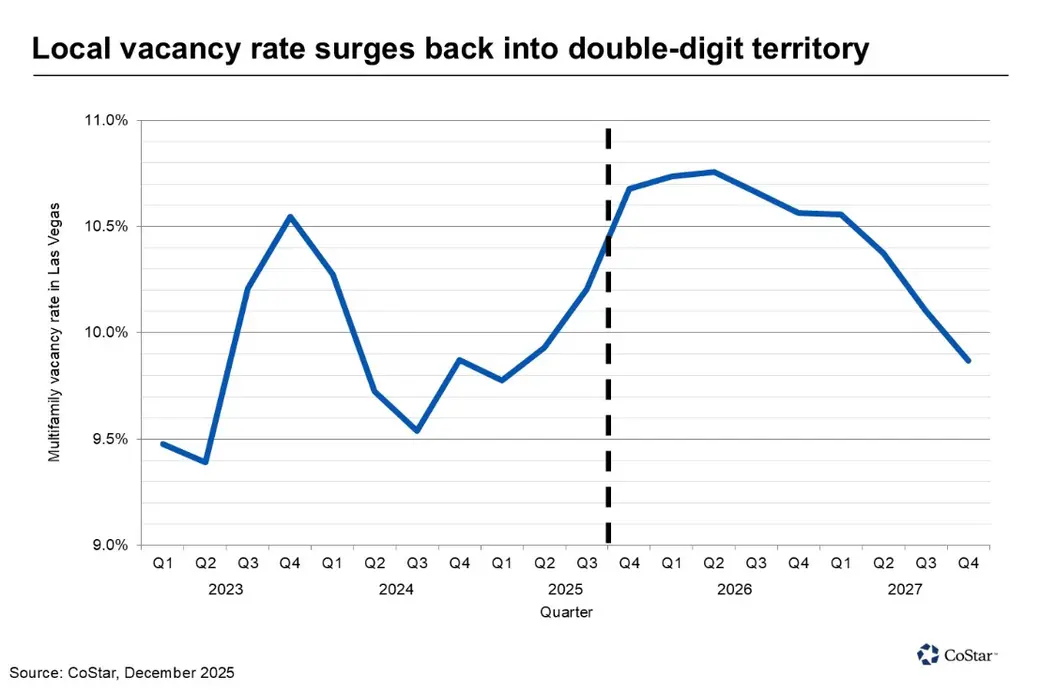

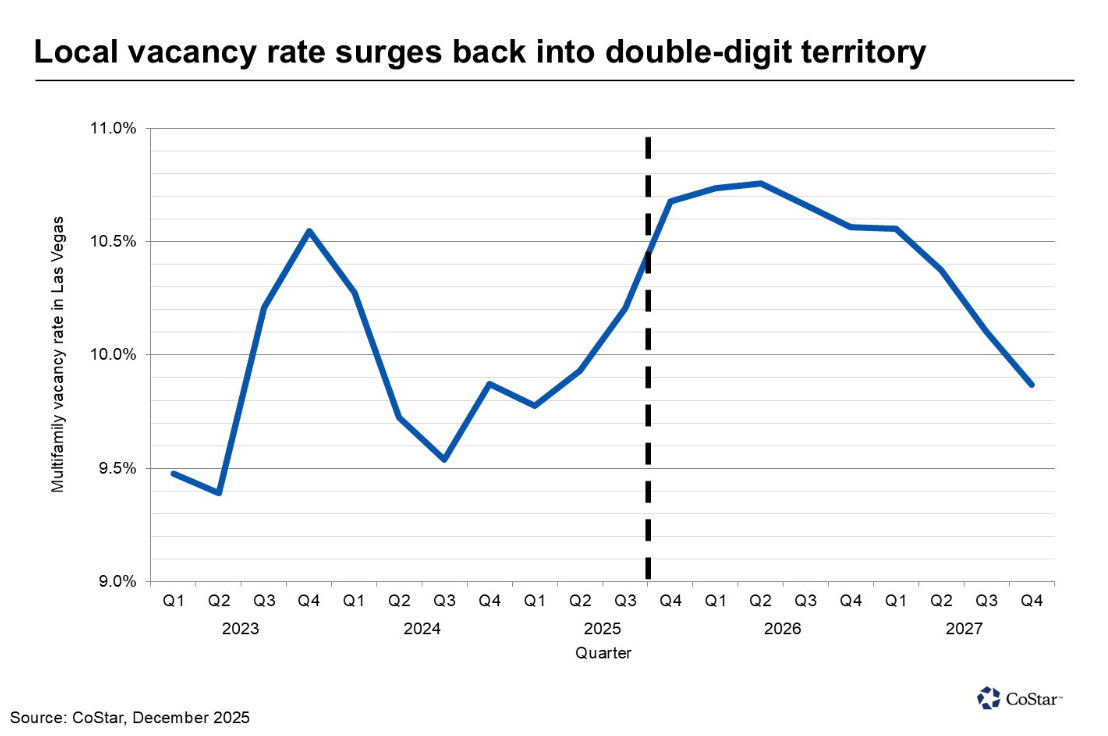

You may have seen recent headlines noting that apartment vacancies in Las Vegas have moved back into double-digit territory. At first glance, that sounds concerning—but context matters.

What we’re seeing is not a broad-based breakdown in rental demand. It’s a very specific, temporary dynamic driven largely by newly delivered communities coming online and leasing up—especially in the higher-end segment. CoStar’s own headline framing notes vacancy breached double digits as “several new communities open their doors.”

In other words: this is primarily a Class A lease-up story, not a citywide demand collapse.

Why Headline Vacancy Can Look Worse Than the Market Feels

When a wave of new supply delivers, many properties open with little or no preleasing and fill over time. That means units hit the market vacant first—then lease up in stages. Even a relatively small number of empty luxury units can push overall vacancy higher, especially when deliveries are concentrated in a short window.

Las Vegas has been in exactly that delivery window.

A Las Vegas Review-Journal report citing CoStar data notes:

-

Net deliveries hit a high mark in 2023 (6,515 units)

-

Approximately 4,600 units were delivered over the prior 12 months (as of May 2025)

-

Valley vacancy was reported at 9.9% in 2024, after rising from 8.6% (2022) to 10.5% (2023)

That’s the math behind the headlines: deliveries surged, and lease-up takes time.

2023 Was the Peak Delivery Year—And That Matters

CoStar market commentary has also described 2023 as a record-setting year for Las Vegas apartment completions, citing 5,600 units completed and calling it an all-time high.

Whether you reference 5,600 or 6,515 depending on dataset definitions (completed vs. net delivered), the takeaway is the same: Las Vegas absorbed an unusually large supply wave over a short period. That raises headline vacancy in the short run even when underlying demand remains active.

The “Rest of Market” Can Be Strong While Class A Leases Up

This is the core nuance investors need:

-

New Class A deliveries often compete aggressively on concessions to fill quickly.

-

Workforce and mid-market housing can remain far more stable because it isn’t competing for the same renter.

-

A renter priced out of homeownership or luxury rents doesn’t disappear—they typically shift into Class B/C demand.

Another factor supporting stability is retention. Nationally, resident retention has been elevated: the National Apartment Association cited findings from Zego’s 2024 Resident Experience Management Report showing 59% of residents planned to renew, the highest since the report began in 2021.

RealPage also reported renewal rates just over 54% for the year-ending October 2024, up year over year.

When renewal behavior strengthens, mid-market communities often rely less on heavy concessions because renters stay put.

Why This Supports the Longer-Term Outlook

Here’s the more important forward-looking point: supply pressure doesn’t stay elevated forever—especially when starts slow.

The same Las Vegas Review-Journal/CoStar reporting noted multifamily construction starts fell sharply (example: 342 starts in Q1 2025 vs. 1,333 in Q1 2024, per the article).

When fewer projects start, fewer deliver later—meaning competition eases after the current lease-up cohort stabilizes.

That’s why today’s headline vacancy can coexist with a constructive longer-term setup:

-

Lease-ups finish

-

Deliveries taper

-

Vacancy compresses

-

Rent pressure normalizes

What This Means for Investors

If you’re buying or holding in Las Vegas, this environment reinforces a practical takeaway:

Well-located Class B and Class C assets can remain fundamentally strong because they’re supported by affordability-driven demand and insulated from the volatility of luxury delivery cycles.

But you only benefit from that strength if your underwriting is specific:

-

Underwrite effective rent, not asking rent (account for concessions)

-

Validate unit-type demand (1BR vs 2–3BR behaves differently)

-

Map nearby deliveries and the true competitive set

-

Stress-test exit cap rates and debt coverage

Headlines can set the mood. The rent roll, the comp set, and the supply map determine performance.

How HYDE Real Estate Group Can Help

At HYDE Real Estate Group, we help clients look past headlines and focus on what actually drives results: submarket dynamics, asset class segmentation, unit-mix reality, and durable demand.

If you’d like to understand how these trends impact your portfolio—or where opportunity is emerging in Las Vegas multifamily—we’re ready to walk through it with you.

-

Request a deal review / underwriting

We’ll stress-test effective rents, concessions, expenses, DSCR sensitivity, break-even occupancy, and the realistic path to upside.

-

Get a submarket rent & vacancy snapshot

We’ll outline competitive pressure, supply risk, concession trends, and where Class B/C fundamentals are strongest.

-

Ask for current B/C value-add opportunities

We’ll share opportunities worth underwriting and the most common, realistic upside angles we’re seeing right now.

FAQ

Why can vacancy rise even if demand is still healthy?

Because new deliveries often open with units vacant and lease up over time. A concentrated wave of openings can push headline vacancy higher temporarily, even if absorption remains active.

Was 2023 really that big of a delivery year in Las Vegas?

Yes—both local reporting and CoStar commentary described 2023 as a record year, with thousands of units completed/delivered.

Does double-digit vacancy mean Las Vegas is in trouble?

Not automatically. It can reflect a lease-up cycle, particularly when new Class A product delivers in volume. The key is whether vacancy is concentrated in new deliveries or spread across stabilized stock.

Why do Class B/C assets often look stronger during Class A lease-ups?

Because they serve a different renter: affordability-driven households, longer tenures, and residents who may be priced out of luxury rents or homeownership. Higher retention can also stabilize occupancy.

What metric should investors focus on instead of headline vacancy?

Look at stabilized occupancy, effective rent (after concessions), renewal vs. new lease spreads, and nearby future deliveries competing in the same segment.

How do concessions distort the market?

Concessions can keep asking rents high while effective rents drop. If you underwrite asking rent, you can overstate NOI and overpay.

What’s the sign that conditions may improve in the next phase?

A slowing construction-start pipeline usually means fewer future deliveries—reducing competitive pressure after the current lease-up cohort absorbs.

Categories

Recent Posts

GET MORE INFORMATION